Understanding the Conventional Mortgage Basics

When you are ready to buy a home in the heartland, choosing the right loan program is crucial. A conventional mortgage is one of the most popular financing options for homebuyers in Des Moines, IA. Unlike government-backed loans, a conventional fixed-rate mortgage is not insured by the federal government. Instead, it is offered by private lenders and often backed by Fannie Mae or Freddie Mac.

At Midwest Family Lending, we know that the mortgage process can feel overwhelming. That is why our experienced mortgage brokers in Metro Des Moines are dedicated to simplifying the process. Whether you are looking for a classic 30-year fixed-rate mortgage or need a trusted advisor to review your current pre-approval, we are experts at providing second opinions on conventional mortgages to ensure you get the best terms possible.

Conforming vs. Non-Conforming Conventional Loans

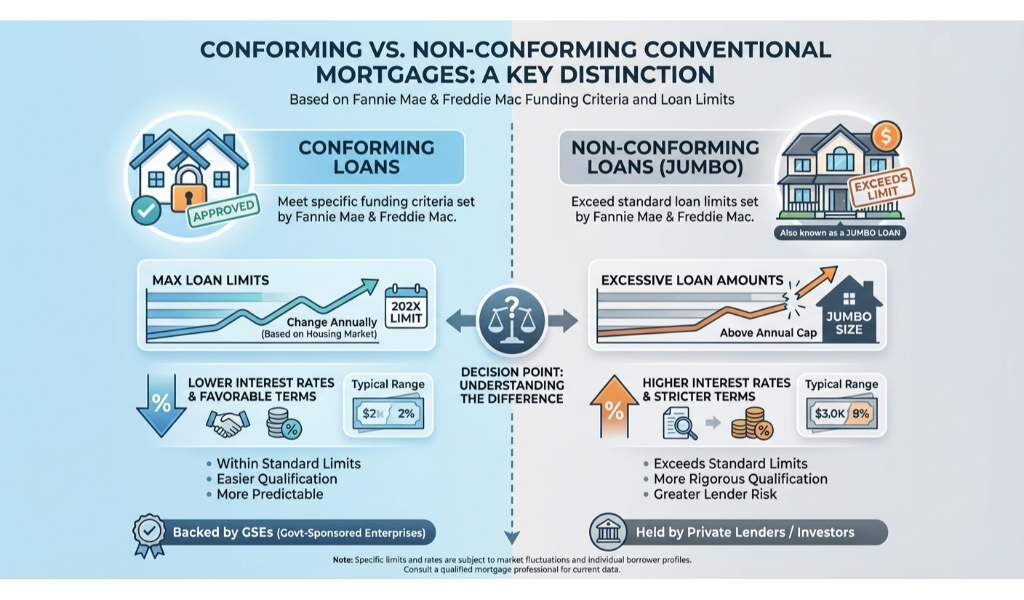

One of the most important distinctions to understand when exploring a conventional mortgage is the difference between conforming and non-conforming loans. A conforming loan meets the specific funding criteria set by Fannie Mae and Freddie Mac, including maximum loan limits that change annually based on the housing market.

- Conforming Loans: These mortgages fall within standard loan limits and typically offer lower interest rates and more favorable terms.

- Non-Conforming Loans: Also known as a jumbo mortgage, these loans exceed the standard limits. They are designed for purchasing luxury properties or homes in highly competitive real estate markets.

Choosing between these two depends largely on your homebuying budget and overall financial profile. Our Des Moines mortgage experts will do a comprehensive review to provide the best options for your overall financial goals.

| Feature | Conforming Conventional Mortgage | Non-Conforming (Jumbo) Mortgage |

|---|---|---|

| Loan Limits | Within FHFA county limits | Exceeds FHFA limits |

| Credit Score Needed | Typically 620 or higher | Usually 700 or higher |

| Down Payment | As low as 3% for first-time buyers | Typically 10% to 20% or more |

| Interest Rates | Generally lower and highly competitive | Slightly higher due to increased lender risk |

Why Choose a Conventional Fixed-Rate Mortgage?

A conventional fixed-rate mortgage offers predictability and peace of mind. Your interest rate and monthly principal and interest payments remain exactly the same for the entire life of the loan. This makes budgeting incredibly straightforward for Midwest families.

While some buyers might benefit from an FHA purchase loan, especially those with lower credit scores or smaller down payments, a conventional mortgage often provides better long-term savings. You can avoid upfront mortgage insurance premiums, and if you put down 20%, you will not have to pay private mortgage insurance (PMI) at all.

As a family-owned lender in Urbandale serving the greater Des Moines area, we treat our customers like family. We pride ourselves on being fast, thorough, and responsive. If you are unsure which path is right for you, remember that we are experts at providing second opinions on conventional mortgages. We will review your scenario and ensure you are positioned for financial success.

Q1: What is a conventional mortgage?

A conventional mortgage is a home loan that is not guaranteed or insured by the federal government. It is typically backed by private lenders and must meet guidelines set by Fannie Mae or Freddie Mac.

Q2: What credit score is needed for a conventional fixed-rate mortgage?

Most lenders require a minimum credit score of 620 for a conventional loan, though a higher score will help you secure a better interest rate.

Q3: How much of a down payment is required?

While many believe you need 20% down, first-time homebuyers can often secure a conventional mortgage with as little as 3% down.

Q4: Can Midwest Family Lending give me a second opinion on my loan estimate?

Yes! We are experts at providing second opinions on conventional mortgages and will gladly review your current offer to see if we can find you better terms in Des Moines.

Q5: How does a conventional loan differ from an FHA loan?

FHA loans are government-backed and often have more lenient credit requirements, while conventional loans are private and generally offer lower costs over time if you have strong credit.Get Your Conventional Mortgage Second Opinion Today