Early Habits to Reduce Stress and Prepare Your Finances

Welcome to the exciting journey of buying a home in Des Moines, IA! The path to homeownership is thrilling, but the financing side can sometimes feel overwhelming. By adopting a few early prep habits, you can reduce stress and ensure everything moves forward with fewer surprises. At Midwest Family Lending, our dedicated team loves helping people get into their dream homes. Let us look at the first steps to take to ensure you are fully prepared.

Assess your financial health: Create a detailed budget that accounts for a down payment, closing costs, and ongoing homeownership expenses like property taxes and insurance.

Build your emergency fund: Aim for three to six months of living expenses saved in a separate account to handle unexpected home repairs or life changes.

Review your credit report: Obtain free copies of your credit reports from all three major bureaus to check for errors and understand your credit standing. Improving your score early can lead to better interest rates.

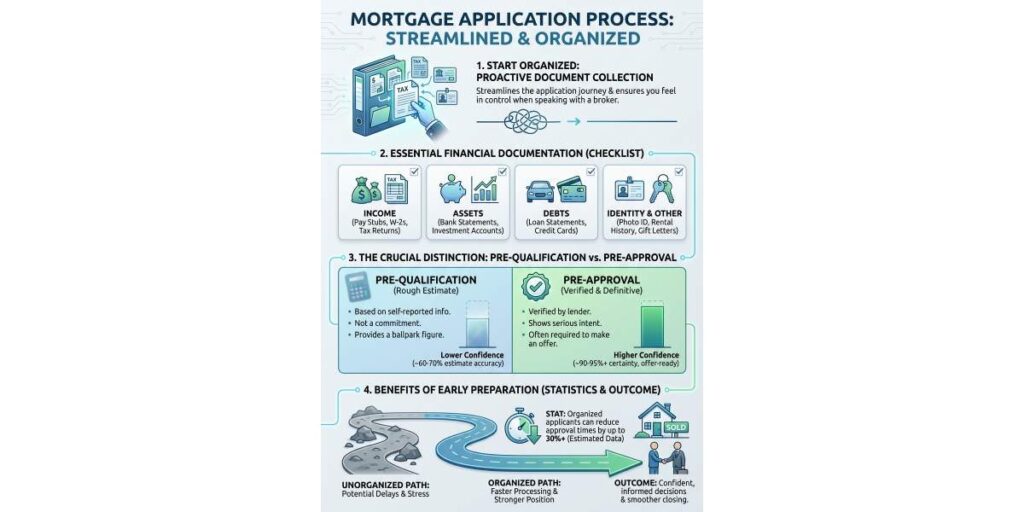

Gathering Documents and Understanding Pre-Approval

The mortgage application process requires specific paperwork. Being organized from the start will make the process much smoother. You will want to proactively collect all necessary financial documentation. This streamlines the application process and helps you feel completely in control when speaking with a mortgage broker.

Moreover, it is vital to understand the difference between pre-qualification and pre-approval. While pre-qualification offers a rough estimate of what you might borrow based on self-reported data, a mortgage pre-approval is a formal process. Getting pre-approved means a lender has verified your finances, which strengthens your offer to sellers and sets a realistic budget. Ready to take that step? Learn more about buying a home with our local experts.

The Power of Clarity: Navigating Des Moines Real Estate with Confidence

When stepping into the Des Moines housing market, the sheer volume of financial data can feel overwhelming. While securing a competitive interest rate is undeniably important, the person guiding you through this complex journey shapes your entire experience. At Midwest Family Lending, we believe that the right advisor provides clarity, ensures efficient timelines, and builds unwavering confidence from your very first conversation through to closing.

For many homebuyers, the world of home financing is a maze of unfamiliar terms and intricate paperwork. A dedicated home financing advisor cuts through the confusion by offering transparent, easy-to-understand explanations. Here is how a trusted professional illuminates your path to homeownership:

Demystifying Loan Options: Your advisor will break down various loan types, such as conventional mortgages, FHA, VA, or USDA loans, explaining the benefits and drawbacks of each in relation to your unique financial situation.

Translating Complex Jargon: Mortgage language can be intimidating. A skilled mortgage broker translates industry jargon into plain language, ensuring you understand every step, term, and document.

Personalized Financial Guidance: Beyond just presenting options, an expert evaluates your overall financial health, assessing credit scores, income stability, and debt-to-income ratios to tailor solutions that genuinely align with your goals.

We are proud to have earned a 5-star reputation in the Des Moines Metro area because we treat our customers like family. You deserve to feel confident and in control of the biggest purchase of your life.

Optimizing Timelines: How the Right Mortgage Expert Keeps You on Track

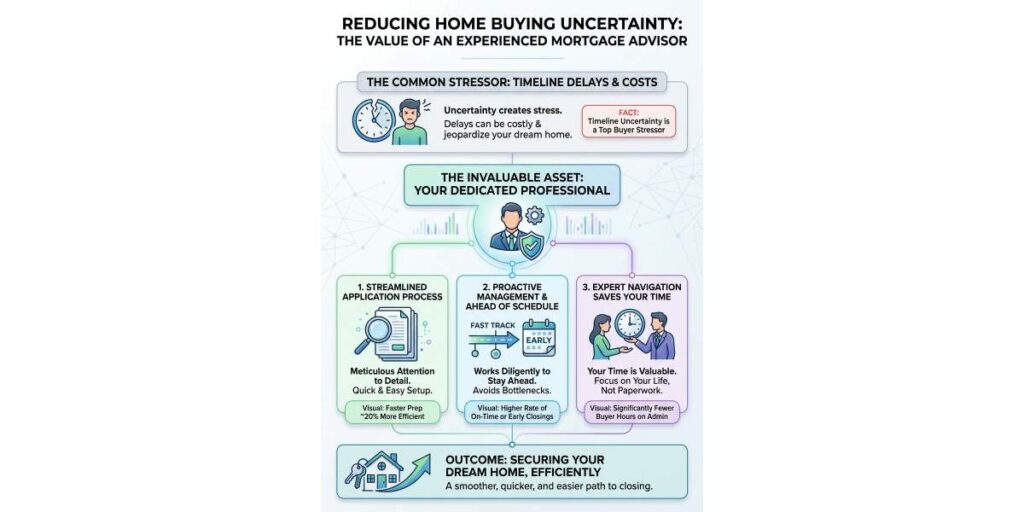

One of the most common stressors in the home buying process is the uncertainty surrounding timelines. Delays can be costly, frustrating, and potentially jeopardize your dream home. This is where an experienced mortgage advisor becomes an invaluable asset. Your time is valuable, and a dedicated professional works diligently to make getting the right mortgage quick, easy, and ahead of schedule whenever possible.

A streamlined application process requires meticulous attention to detail. Your advisor takes on the heavy lifting, from helping you organize and verify essential financial documents to submitting paperwork efficiently. They act as a central point of contact, coordinating seamlessly with real estate agents, underwriters, and closing agents. Realtors and other real estate professionals consistently recommend working with our team because we have a track record of working behind the scenes to make mortgage magic happen.

Furthermore, proactive problem solving is a hallmark of a great advisor. With deep knowledge of the lending landscape, they anticipate potential hurdles and address them before they become roadblocks. By setting realistic expectations from the outset, your advisor minimizes surprises and ensures a smooth, predictable journey to the closing table.

When you are ready to buy a home in the heartland, choosing the right loan program is crucial. A conventional mortgage is one of the most popular financing options for homebuyers in Des Moines, IA. Unlike government-backed loans, a conventional fixed-rate mortgage is not insured by the federal government. Instead, it is offered by private lenders and often backed by Fannie Mae or Freddie Mac.

At Midwest Family Lending, we know that the mortgage process can feel overwhelming. That is why our experienced mortgage brokers in Metro Des Moines are dedicated to simplifying the process. Whether you are looking for a classic 30-year fixed-rate mortgage or need a trusted advisor to review your current pre-approval, we are experts at providing second opinions on conventional mortgages to ensure you get the best terms possible.

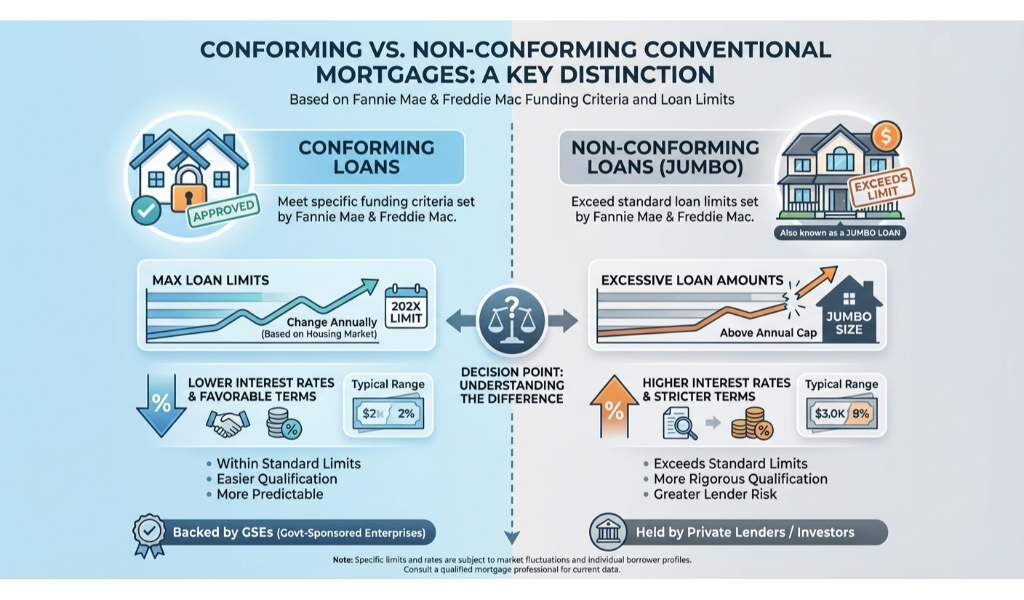

Conforming vs. Non-Conforming Conventional Loans

One of the most important distinctions to understand when exploring a conventional mortgage is the difference between conforming and non-conforming loans. A conforming loan meets the specific funding criteria set by Fannie Mae and Freddie Mac, including maximum loan limits that change annually based on the housing market.

Conforming Loans: These mortgages fall within standard loan limits and typically offer lower interest rates and more favorable terms.

Non-Conforming Loans: Also known as a jumbo mortgage, these loans exceed the standard limits. They are designed for purchasing luxury properties or homes in highly competitive real estate markets.

Choosing between these two depends largely on your homebuying budget and overall financial profile. Our Des Moines mortgage experts will do a comprehensive review to provide the best options for your overall financial goals.

Feature

Conforming Conventional Mortgage

Non-Conforming (Jumbo) Mortgage

Loan Limits

Within FHFA county limits

Exceeds FHFA limits

Credit Score Needed

Typically 620 or higher

Usually 700 or higher

Down Payment

As low as 3% for first-time buyers

Typically 10% to 20% or more

Interest Rates

Generally lower and highly competitive

Slightly higher due to increased lender risk

Why Choose a Conventional Fixed-Rate Mortgage?

A conventional fixed-rate mortgage offers predictability and peace of mind. Your interest rate and monthly principal and interest payments remain exactly the same for the entire life of the loan. This makes budgeting incredibly straightforward for Midwest families.

While some buyers might benefit from an FHA purchase loan, especially those with lower credit scores or smaller down payments, a conventional mortgage often provides better long-term savings. You can avoid upfront mortgage insurance premiums, and if you put down 20%, you will not have to pay private mortgage insurance (PMI) at all.

As a family-owned lender in Urbandale serving the greater Des Moines area, we treat our customers like family. We pride ourselves on being fast, thorough, and responsive. If you are unsure which path is right for you, remember that we are experts at providing second opinions on conventional mortgages. We will review your scenario and ensure you are positioned for financial success.

Q1: What is a conventional mortgage?

A conventional mortgage is a home loan that is not guaranteed or insured by the federal government. It is typically backed by private lenders and must meet guidelines set by Fannie Mae or Freddie Mac.

Q2: What credit score is needed for a conventional fixed-rate mortgage?

Most lenders require a minimum credit score of 620 for a conventional loan, though a higher score will help you secure a better interest rate.

Q3: How much of a down payment is required?

While many believe you need 20% down, first-time homebuyers can often secure a conventional mortgage with as little as 3% down.

Q4: Can Midwest Family Lending give me a second opinion on my loan estimate?

Yes! We are experts at providing second opinions on conventional mortgages and will gladly review your current offer to see if we can find you better terms in Des Moines.

Q5: How does a conventional loan differ from an FHA loan?

FHA loans are government-backed and often have more lenient credit requirements, while conventional loans are private and generally offer lower costs over time if you have strong credit.Get Your Conventional Mortgage Second Opinion Today

If you currently have an FHA loan, an FHA streamline refinance might be the perfect tool to lower your interest rate and reduce your monthly payment. At Midwest Family Lending in Des Moines, IA, we specialize in helping local homeowners navigate the mortgage process with ease. The FHA Streamline Refi program is designed to be fast and efficient, requiring significantly less documentation than a traditional rate and term refinance.

One of the biggest advantages of an FHA Streamline is that it often does not require a home appraisal. This means you can take advantage of better market conditions quickly. Whether you are looking for your first mortgage adjustment or you want us to review a current offer, our mortgage brokers are experts at providing second opinions on FHA streamline refinance options.

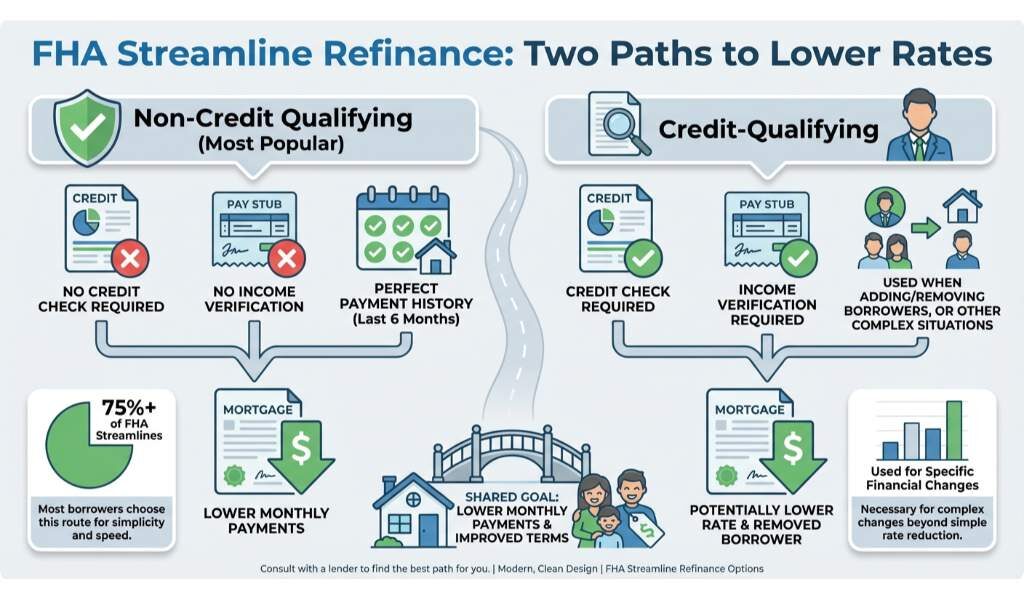

Credit-Qualifying vs. Non-Credit Qualifying FHA Streamlines

When considering an FHA streamline refinance, it is important to understand the two main paths available to borrowers. The Federal Housing Administration offers both credit-qualifying and non-credit qualifying options to suit different financial situations.

Non-Credit Qualifying: This is the most popular route. It does not require a credit check or income verification. As long as you have a perfect payment history on your current FHA loan for the past six months, you can generally qualify.

Credit-Qualifying: This option requires the lender to verify your income and credit score. Borrowers typically choose this path if a change in the mortgage term results in a higher monthly payment or if a borrower is being removed from the loan.

If you are a veteran exploring other financing options, you might also be interested in a VA Interest Rate Reduction Refinance Loan (IRRRL). However, for FHA borrowers, the streamline program remains the most efficient choice.

Feature

Non-Credit Qualifying

Credit-Qualifying

Credit Check Required

No

Yes

Income Verification

No

Yes

Appraisal Needed

Typically No

Typically No

Best For

Lowering interest rate easily

Removing a borrower from the loan

Why Choose Midwest Family Lending for Your FHA Streamline Refi?

Choosing the right mortgage broker in the Des Moines Metro area can make all the difference. At Midwest Family Lending, mortgages are not just one thing we do; they are all we do. We pride ourselves on offering fast, thorough, and responsive service to our Iowa community.

We know that navigating loan terms can be overwhelming. That is why we are experts at providing second opinions on FHA streamline refinance offers. If you have a quote from another lender, bring it to us. We will review it transparently to ensure you are getting the best possible deal for your overall financial goals.

Q1: What is an FHA Streamline Refinance?

It is a simplified refinance program for existing FHA homeowners designed to lower interest rates and monthly payments with minimal documentation.

Q2: Do I need an appraisal for an FHA Streamline Refi?

In most cases, no appraisal is required. This saves you time and money during the refinance process.

Q3: Can I get cash out with an FHA Streamline?

No, the streamline program is strictly for lowering your rate or changing your loan term. It does not allow borrowers to take cash out.

Q4: How long does the FHA Streamline process take?

Because it requires less paperwork, an FHA Streamline can often close much faster than a traditional refinance, typically within 30 to 45 days.

Q5: Where can I get a second opinion on my FHA Streamline offer in Des Moines?

Midwest Family Lending offers expert second opinions to ensure you receive the most competitive terms available for your unique financial situation.

Navigating First-Time Buyer Loans with Midwest Family Lending

Buying your very first home is one of the most exciting milestones in life. However, finding the right first time homebuyer mortgage can feel overwhelming. At Midwest Family Lending in Des Moines, IA, we understand the local real estate landscape. Our goal is to simplify the process so you feel confident and in control of your biggest purchase.

When exploring a First-Time Home Buyer Mortgage, it is crucial to know all your options. Whether you need a low down payment solution or flexible credit requirements, there are specific First-Time Buyer Loans designed just for you. If you have already started the process elsewhere, remember that we are experts at providing second opinions on first-time homebuyer mortgages. We will review your current offer to ensure you are getting the best possible terms. You might also want to explore an FHA purchase loan, which is highly popular among new buyers for its flexible qualification standards.

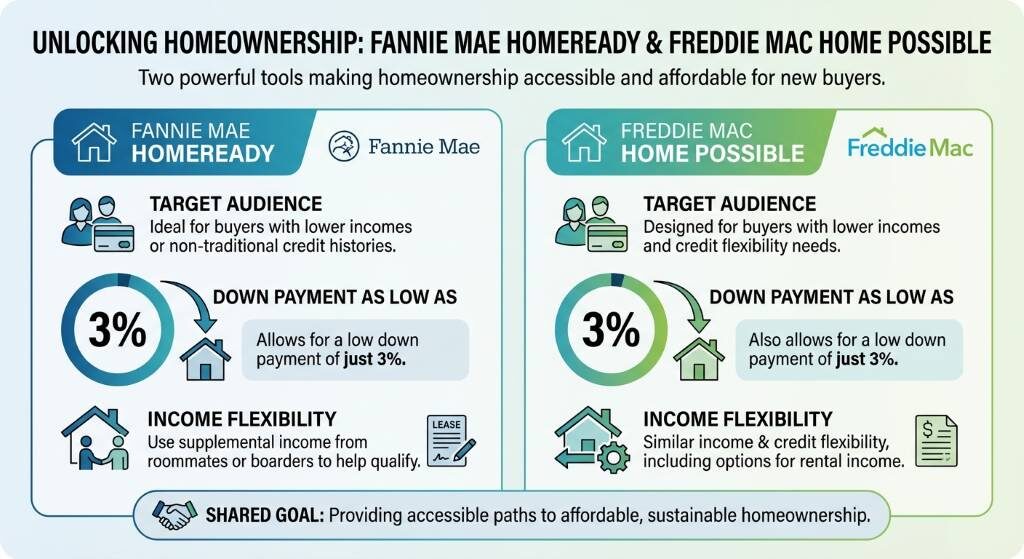

Top First-Time Homebuyer Mortgage Programs: HomeReady and Home Possible

Two of the most powerful tools for new buyers are the Fannie Mae HomeReady and Freddie Mac Home Possible programs. Both are designed to make homeownership more accessible and affordable.

HomeReady: This program is ideal for buyers with lower incomes or those who have non-traditional credit histories. It allows for a down payment as low as 3 percent. Additionally, you can use supplemental income from roommates or boarders to help you qualify.

Home Possible: Similar to HomeReady, this Freddie Mac program also requires just a 3 percent down payment. It is specifically tailored for very low to low-income borrowers. A major benefit is that your down payment can come entirely from a gift or grant.

Pairing these conventional programs with down payment assistance programs can drastically reduce your out-of-pocket expenses at closing. Because these options have specific income limits and property requirements, consulting with a knowledgeable mortgage broker in the Des Moines Metro area ensures you select the perfect fit for your financial puzzle.

Program Feature

HomeReady (Fannie Mae)

Home Possible (Freddie Mac)

Standard FHA Loan

Minimum Down Payment

3%

3%

3.5%

Minimum Credit Score

Typically 620

Typically 660

600 (for 3.5% down)

Income Limits

Yes (80% of Area Median Income)

Yes (80% of Area Median Income)

None

Mortgage Insurance

Reduced rates available; cancelable

Reduced rates available; cancelable

Required for the life of the loan

Why Get a Second Opinion on Your Home Loan?

Rates are not everything when it comes to securing a first time homebuyer mortgage. A thorough, comprehensive review of your financial goals is essential. At Midwest Family Lending, our mortgage brokers are dedicated to looking out for your best interests. We are proud of our 5-star reputation for being trustworthy and treating our customers like family.

We highly encourage new buyers to seek a second opinion. Sometimes, another lender might miss a critical detail or fail to inform you about beneficial First-Time Buyer Loans. We will proactively review your scenario, explain your options clearly, and ensure you are not leaving money on the table. Our fast, responsive team works behind the scenes to make mortgage magic happen for you.

Q1: What qualifies someone for a first time homebuyer mortgage?

Generally, you are considered a first-time homebuyer if you have not owned a principal residence within the past three years. This status opens the door to specialized First-Time Buyer Loans and assistance programs.

Q2: How much of a down payment do I need for a First-Time Home Buyer Mortgage?

While many believe you need 20 percent down, programs like HomeReady and Home Possible allow for as little as 3 percent down. Other options like FHA loans require just 3.5 percent.

Q3: What is the difference between HomeReady and Home Possible?

Both offer 3 percent down payment options for lower-income borrowers. HomeReady is backed by Fannie Mae and allows income from non-borrower household members to help you qualify. Home Possible is backed by Freddie Mac and offers similar benefits but has slightly different credit and income calculation guidelines.

Q4: Can I get a second opinion on my first-time homebuyer mortgage?

Absolutely. We are experts at providing second opinions on first-time homebuyer mortgages. We will review your current pre-approval to ensure you are receiving the best rates and lowest fees possible.

Q5: Are there programs to help with my down payment in Des Moines?

Yes, there are numerous local and state down payment assistance programs available in Iowa. We can help you find and apply for these grants or secondary loans to lower your upfront costs.

If you are looking to buy a home in the Des Moines metro area, an FHA loan might be the perfect path to homeownership. Backed by the Federal Housing Administration, an FHA purchase loan is designed to help buyers secure financing with more flexible qualification requirements compared to other mortgage options.

Whether you are entering the market for the first time or simply looking for a more accessible financing route, exploring first-time homebuyer mortgage options alongside an FHA loan can open doors to your dream home. At Midwest Family Lending, we specialize in helping Iowa families navigate these choices with confidence.

Lower minimum down payment requirements

More forgiving credit score thresholds

Competitive interest rates

We are also experts at providing second opinions on FHA purchase loans. If you have already received a quote and want to ensure you are getting the best terms possible, our local mortgage brokers are here to review your options.

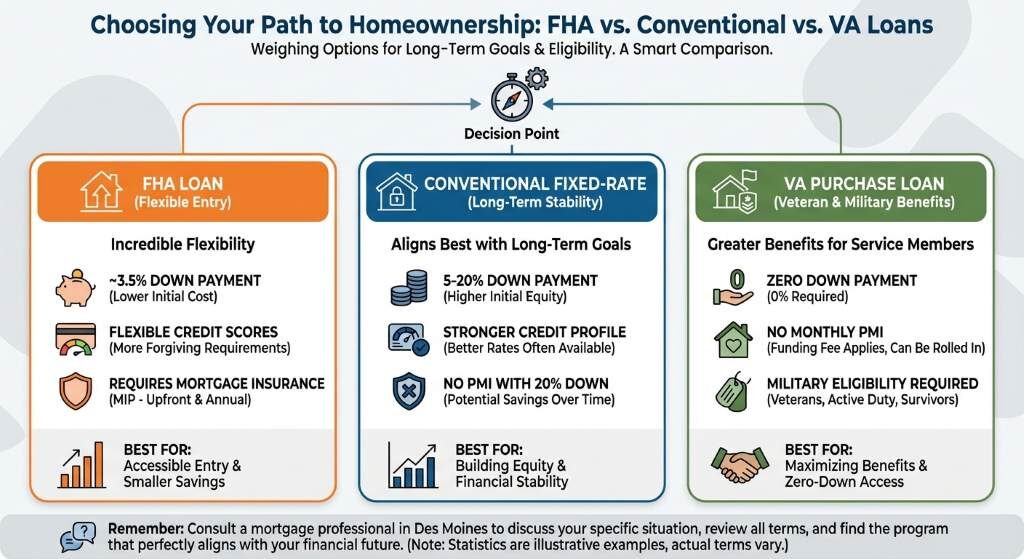

Comparing FHA Loans to Other Mortgage Options

Choosing the right mortgage program requires understanding how an FHA loan stacks up against other popular financing methods. While an FHA purchase loan offers incredible flexibility, it is always smart to weigh it against a conventional fixed-rate mortgage to see which aligns best with your long-term financial goals.

For our military veterans and active-duty service members in Des Moines, a VA purchase loan might provide even greater benefits, such as zero down payment requirements. However, for many civilian buyers, the FHA loan remains the most accessible route to homeownership. Let us look at a quick breakdown of how these programs compare.

Loan Type

Minimum Down Payment

Minimum Credit Score (Typical)

Best For

FHA Loan

3.5%

580

Buyers with limited down payment funds or lower credit scores

Conventional Loan

3% to 5%

620

Buyers with strong credit and a larger down payment

VA Loan

0%

No strict minimum (often 580+)

Eligible veterans and active military personnel

Why Choose Midwest Family Lending for Your FHA Loan

At Midwest Family Lending, our mortgage brokers in the Des Moines metro area are dedicated to simplifying the mortgage process. Mortgages are not just one thing we do; they are all we do. We understand that buying a home is a massive financial milestone, and you deserve a team that treats you like family.

If you are currently working with another lender but feel uncertain about the terms, remember that we are experts at providing second opinions on FHA purchase loans. A quick review of your current offer by our experienced team could save you thousands of dollars over the life of your loan. We provide a thorough, responsive, and fast experience tailored to the unique Des Moines real estate market.

Q1: What is the minimum down payment for an FHA purchase loan?

The minimum down payment for an FHA loan is typically 3.5% of the purchase price, provided you have a credit score of at least 600. If you have 10% down, you can go down to a 580 credit score.

Q2: Can I use gift funds for my FHA loan down payment?

Yes, FHA guidelines allow borrowers to use 100% gift funds from an approved donor, such as a family member, to cover the down payment and closing costs.

Q3: Are FHA loans only for first-time homebuyers?

No, FHA loans are available to both first-time buyers and repeat buyers. They are simply popular among first-time buyers due to their flexible qualification requirements.

Q4: How do I know if I am getting the best FHA loan rate?

The best way to ensure you are getting a competitive rate is to get a second opinion. Midwest Family Lending specializes in reviewing existing FHA purchase loan offers to find you the best possible terms.

Q5: Do FHA loans require mortgage insurance?

Yes, FHA loans require both an upfront mortgage insurance premium and an annual mortgage insurance premium, which is typically rolled into your monthly payments.

Local Knowledge Translates to Better Mortgage Program Selection

When you are ready to buy a home in the heartland, the team you choose to guide you makes all the difference. The Midwest features a highly unique real estate landscape. From the bustling, fast-paced neighborhoods of the Des Moines metro to the expansive rural properties across Iowa, Nebraska, South Dakota, and Colorado, having a family-owned lender in Urbandale in your corner ensures you receive advice tailored to your specific needs.

Unlike national mega-banks that treat you like a number on a spreadsheet, Midwest Family Lending treats you like family. Our local mortgage brokers understand the precise nuances of the Midwest market. We know that property taxes in Polk County differ drastically from those in rural Nebraska, and we know exactly how local agricultural zoning can impact your loan options.

Deep Local Roots: We live and work in the exact communities we serve.

Tailored Program Selection: We match your long-term financial goals with the perfect loan product.

Unmatched Trust: We proudly maintain a 5-star reputation for putting our clients first.

Navigating Rural and Urban Real Estate in the Midwest

Navigating the mortgage process can feel overwhelming, but our dedicated team of mortgage experts is here to simplify it. A one-size-fits-all approach simply does not work for Midwest real estate. Because our team understands both urban and rural markets deeply, we can expertly guide you toward the absolute best program for your situation.

For example, if you are looking at a property outside the Des Moines city limits, you might qualify for a zero-down USDA Rural Development loan. Conversely, if you want to refinance your mortgage in a suburban neighborhood to take advantage of lower interest rates or shorten your loan term, a conventional loan might be your best path forward. Rates are not everything; we do a comprehensive review to provide the best options for your overall financial goals.

Loan Program

Best For

Location Suitability

Typical Down Payment

Conventional Loans

Buyers with strong credit profiles

Des Moines Metro & Suburbs

As low as 3%

USDA Rural Development

Low-to-moderate income buyers

Rural Iowa, NE, SD, CO

0% Down

FHA Loans

First-time homebuyers

Urban & Suburban Areas

3.5% Down

VA Loans

Veterans and active military

All Midwest Regions

0% Down

Why Choose a Family-Owned Mortgage Broker in Urbandale?

Choosing a family-owned mortgage broker in Urbandale means you get a team that is fast, thorough, and highly responsive. Your time is valuable, and we make getting the right mortgage quick and easy, often staying well ahead of schedule. Local realtors and real estate professionals consistently recommend working with us because of our proven track record of making mortgage magic happen behind the scenes.

If you are ready to get your ducks in a row, our licensed home loan originators are ready to help you reach your dreams. Mortgages are not just one thing we do; they are ALL we do. We look out for your best interests, helping with everything from starter houses to retirement homes, and refinancing along the way.

Disclaimer: This content is for informational purposes only. Midwest Family Lending is an Equal Housing Lender. Please consult with a licensed loan originator for specific rates and program eligibility. For more information, contact us at info@midwestfamilylending.com or call 1-515-252-7107.

Q1: Why should I choose a local mortgage broker in Des Moines over a large national bank?

A local mortgage broker offers personalized service and deep knowledge of the local real estate market. We understand regional property taxes, local loan programs, and community-specific nuances that national banks often overlook.

Q2: Does Midwest Family Lending only serve the Des Moines metro area?

While we are proudly based in Urbandale and serve the greater Des Moines metro, our expertise extends far beyond. We provide home loan solutions across rural Iowa, Nebraska, South Dakota, and Colorado.

Q3: Can you help me find a loan for a rural property?

Absolutely. We have extensive experience with rural properties and can help you navigate specialized programs, such as USDA Rural Development loans, which are perfect for eligible properties in rural Midwest areas.

Q4: What is the first step to buying a home with Midwest Family Lending?

The first step is to get your ducks in a row by reaching out to one of our licensed home loan originators. We will review your financial goals, discuss your options, and help you get pre-approved so you can shop with confidence.

Q5: Is it a good time to refinance my mortgage?

Refinancing can be a smart move if you want to lower your monthly payment, shorten your loan term, or tap into your home equity. Our team can provide a comprehensive review of your current mortgage to see if refinancing aligns with your long-term financial goals.

Welcome to 2026, where the landscape of home buying in Des Moines, IA has transformed to become faster, smarter, and more inclusive. For prospective homeowners in Iowa, the days of endless paper trails are fading as AI-powered mortgage applications take center stage. These advanced tools allow lenders to analyze financial data in real-time, drastically reducing the time from application to approval.

However, technology is only half the story. At Midwest Family Lending, we believe in combining these high-tech efficiencies with our signature “high-touch” service. Whether you are looking to buy a home in Urbandale or refinance in the greater Des Moines metro, understanding how these 2026 trends impact your borrowing power is essential. While algorithms speed up the process, our team ensures you find a loan that fits your life—treating you like family, not just a data point.

Unlocking Doors for the Self-Employed: Non-QM Loans

One of the most significant shifts in the 2026 mortgage market is the rise of Non-QM (Non-Qualified Mortgage) loans. These are specifically designed for borrowers who don’t fit the traditional mold—particularly the growing community of self-employed entrepreneurs, freelancers, and gig economy workers in Central Iowa.

Unlike conventional loans that rely heavily on tax returns—which often don’t reflect a business owner’s true cash flow due to write-offs—Non-QM options like Bank Statement Loans allow you to qualify based on actual deposits. This opens the door for many Des Moines business owners to purchase their dream homes without the headache of strict income verification hurdles. By leveraging AI to analyze bank statements quickly, we can determine your purchasing power accurately and efficiently.

Feature

Traditional Conventional Loan

Non-QM / Bank Statement Loan

Ideal Borrower

W-2 Employees, Fixed Income

Self-Employed, Freelancers, Investors

Income Verification

Tax Returns & Pay Stubs

12-24 Months Personal/Business Bank Statements

Debt-to-Income (DTI)

Strict limits (usually max 43-50%)

Flexible DTI ratios allowed

Processing Speed (2026)

Fast (AI-Assisted)

Moderate to Fast (AI-Analyzed)

Loan Limits

Conforming Limits apply

Often higher limits (Jumbo options available)

Why Local Expertise Matters in an AI World

While AI-powered applications can crunch numbers instantly, they cannot replace the strategic advice of a local expert. Algorithms don’t know the nuances of the Urbandale housing market or the specific property tax advantages in different Iowa counties. That is where Midwest Family Lending steps in.

We use technology to handle the busy work, freeing up our licensed home loan originators to focus on you. We help you navigate complex scenarios, from utilizing VA loan benefits to structuring a Non-QM loan that aligns with your long-term financial goals. In 2026, the best mortgage experience is a hybrid one: the speed of modern tech backed by a team that lives in your community and cares about your success.

Q1: What is a Non-QM loan and who is it for?

Non-QM (Non-Qualified Mortgage) loans are for borrowers who don’t meet standard federal lending guidelines, such as self-employed individuals who write off significant expenses on their taxes but have strong cash flow.

Q2: How does AI improve the mortgage process in 2026?

AI speeds up underwriting by instantly analyzing financial documents and bank statements, reducing errors and cutting down the time it takes to get a pre-approval.

Q3: Can I get a mortgage if I am self-employed in Des Moines?

Absolutely. With options like Bank Statement Loans, we can use your business deposits to verify income rather than relying solely on tax returns.

Q4: Are mortgage rates expected to change in 2026?

While market predictions vary, 2026 is seeing a stabilizing trend. Working with a local broker helps you lock in the best rate at the right moment.

Q5: Why choose a local broker over an online-only lender?

Navigating the 2026 Housing Market: Is Your Dream Home Within Reach?

If you have been watching the housing market over the last few years, you know that affordability has been a major hurdle. However, as we move into 2026, the landscape for first-time homebuyers in Des Moines, IA is shifting. With market stabilization on the horizon and projected interest rate adjustments, the window of opportunity is opening again.

At Midwest Family Lending, we understand that buying your first home is likely the biggest financial decision of your life. It can feel like herding cats, but our goal is to help you “get your ducks in a row.” Whether you are looking in Urbandale, Ankeny, or right here in the heart of Des Moines, having a strategic roadmap is essential to overcoming affordability challenges. This guide will walk you through leveraging assistance programs and smart financing to turn your homeownership dream into a reality this year.

Unlocking Iowa Down Payment Assistance & Smart Financing

One of the biggest myths we hear is that you need a 20% down payment to buy a home. In 2026, that simply isn’t true. There are numerous Iowa assistance programs and loan structures designed to help you bridge the affordability gap.

Iowa Finance Authority (IFA) Programs: These programs often provide grants or second mortgages to cover down payments and closing costs for eligible first-time buyers.

FHA Loans: A popular choice for first-time buyers, requiring as little as 3.5% down with more flexible credit requirements.

VA Home Loans: For our veterans and active-duty service members in Urbandale and beyond, VA loans offer 0% down payment options and no private mortgage insurance (PMI).

USDA Rural Development Loans: If you are looking just outside the immediate Des Moines metro, you might qualify for 100% financing.

Smart financing isn’t just about the rate; it’s about looking at your overall financial goals. We act as your “personal loan shoppers,” comparing lenders to find the specific program that lowers your monthly payment and cash-to-close requirements.

Loan Program

Min. Down Payment

Ideal For

Key Benefit

Conventional First-Time

3%

Strong Credit Score (640+)

Cancelable PMI once equity is reached

FHA Loan

3.5%

Credit Challenges or Low Savings

Flexible qualification standards

VA Loan

0%

Veterans & Active Military

No PMI & competitive interest rates

USDA Loan

0%

Rural/Suburban Buyers

100% financing in eligible areas

The Local Advantage: Why ‘Family’ Matters in Your Search

In a fluctuating market, who you work with matters. Unlike big box online lenders, a local Des Moines mortgage broker understands the nuances of our local real estate taxes, insurance costs, and neighborhood values. We don’t just work here; we live here too.

At Midwest Family Lending, we strive to create “Customers for Life.” Our team of licensed home loan originators has decades of experience helping Iowans navigate complex markets. We proactively communicate with you and your Realtor to ensure you are confident and in control. Don’t wait on the sidelines wondering if you can afford a home in 2026—let us run the numbers and show you the possibilities.

Q1: How much income do I need to buy a home in Des Moines in 2026?

It depends on your debt-to-income ratio and the home price. Generally, lenders look for a housing payment that doesn’t exceed 28-31% of your gross monthly income, but programs vary.

Q2: What is the minimum credit score for a first-time homebuyer?

While it varies by program, FHA loans can accept scores as low as 580. Conventional loans typically require a score of 640 or higher for the best rates.

Q3: Are there grants specifically for first-time buyers in Iowa?

Yes! The Iowa Finance Authority (IFA) offers the FirstHome program which can be combined with down payment assistance grants. We can help check your eligibility.

Q4: Should I wait for interest rates to drop further before buying?

Waiting can be risky because if rates drop significantly, home prices often rise due to increased demand. It is often better to secure a home you can afford now and refinance later.

Q5: How do I get pre-approved with Midwest Family Lending?

It’s easy! You can complete our quick online form to get started. We will review your info and help you get your ducks in a row fast.

Is 2026 the Right Time to Refinance Your Des Moines Home?

As we navigate through 2026, the real estate landscape in Des Moines, IA is shifting. After a period of volatility, mortgage rates are stabilizing, creating a window of opportunity for homeowners who bought during the peak rate spikes of previous years. If you are sitting on a mortgage rate higher than current market averages, now is the critical moment to evaluate your options.

At Midwest Family Lending, we understand that your home is likely your biggest financial asset. Whether you want to lower your monthly payment, shorten your loan term, or access equity for home improvements, timing is everything. With experts predicting rates to settle into a more favorable range, refinancing could save you thousands over the life of your loan.

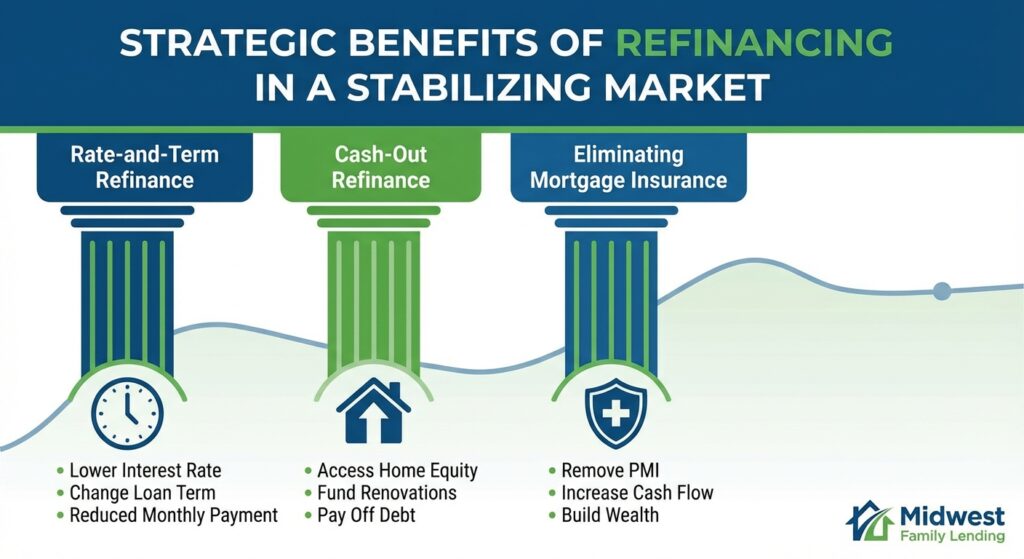

Strategic Benefits of Refinancing in a Stabilizing Market

Refinancing isn’t just about getting a lower interest rate; it’s about aligning your mortgage with your long-term financial goals. Here are the primary strategies for 2026:

Rate-and-Term Refinance: This is the most common method, designed to lower your interest rate or change the loan term (e.g., from 30 years to 15 years) without changing the loan amount significantly.

Cash-Out Refinance: With home values in the Des Moines metro area remaining strong, you may have built significant equity. A cash-out refinance allows you to tap into that wealth to pay off high-interest debt or fund renovations.

Eliminating Mortgage Insurance: If your home’s value has increased and you have over 20% equity, refinancing can help you remove costly Private Mortgage Insurance (PMI).

Our team of mortgage brokers in Urbandale acts as your personal loan shoppers, comparing offers from multiple lenders to ensure you get the best deal possible. Unlike big banks, we work for you, not the lender.

Loan Amount

Current Rate (7.25%)

Refinance Rate (6.00%)

Monthly Savings

Annual Savings

$250,000

$1,705

$1,499

$206

$2,472

$350,000

$2,387

$2,098

$289

$3,468

$450,000

$3,069

$2,698

$371

$4,452

Why Partner with Midwest Family Lending?

Choosing the right partner is just as important as choosing the right loan. At Midwest Family Lending (NMLS #4622), we have been serving the Des Moines community for over 25 years. We pride ourselves on being trustworthy, experienced, and responsive.

We don’t just look at rates; we conduct a comprehensive review of your financial picture. As a local broker, we have specialized knowledge of the Iowa market that national call centers simply can’t match. Whether you are in Urbandale, West Des Moines, or anywhere in Central Iowa, we are here to guide you from application to closing.

Don’t let the cost of waiting eat into your savings. Even a small reduction in rates can translate into significant wealth retention over time.

Q1: How do I know if refinancing is right for me?

A general rule of thumb is if you can lower your interest rate by 0.75% to 1% or more, it is worth investigating. However, we can help you calculate your specific break-even point.

Q2: What is the difference between a mortgage broker and a bank?

A bank can only offer their own products. As a mortgage broker, Midwest Family Lending shops multiple lenders to find the best rates and terms tailored to your specific needs.

Q3: Can I refinance if I have bad credit?

It is possible. We have access to various loan programs, including FHA and VA loans, which often have more flexible credit requirements than conventional loans.

Q4: How long does the refinance process take?

Typically, a refinance takes 30 to 45 days from application to closing, though our team works diligently to make the process as fast and efficient as possible.

Q5: What are the closing costs for refinancing?

Closing costs vary but generally range from 1% to 4% of the loan amount. In many cases, these costs can be rolled into your new loan so you don’t have to pay out of pocket.