If you are a Veteran, active-duty service member, or a surviving spouse living in Urbandale, Iowa, or the greater Des Moines metro area, you may have access to one of the most powerful home financing tools on the market: the VA Home Loan. At Midwest Family Lending, we believe that after you have served our country, it is our honor to serve you by helping you achieve the American Dream of homeownership.

The VA loan program offers incredible benefits, including $0 down payment, no private mortgage insurance (PMI), and competitive interest rates. However, a common question we hear from local veterans is simply: “How do I know if I actually qualify?”

Navigating government requirements can feel overwhelming, but it doesn’t have to be. As your trusted local mortgage experts in Urbandale, we are here to break down the eligibility requirements, financial standards, and the steps you need to take to get the keys to your new home.

The Two Pillars of Qualification: Service and Financials

Qualifying for a VA loan isn’t just about having served in the military; it is a two-step process. First, you must meet the specific service requirements set by the Department of Veterans Affairs (VA). Second, you must meet the financial credit and income standards set by the lender. Let’s break these down.

1. Service Eligibility Requirements

To be eligible for a VA home loan, your service history must meet certain criteria regarding the length and character of your service. Generally, you may be eligible if you meet one of the following conditions:

- Active Duty Service Members: You have served at least 90 continuous days on active duty.

- Veterans: The length of service required depends on when you served (wartime vs. peacetime). Generally, this ranges from 90 days in wartime to 181 continuous days in peacetime.

- National Guard and Reserves: You have completed at least 6 years of service in the National Guard or Reserves, or served 90 days of active duty (at least 30 of which were consecutive).

- Surviving Spouses: You are the un-remarried surviving spouse of a Veteran who died in service or from a service-connected disability.

Note: You must have received a discharge other than dishonorable to be eligible.

2. The “Golden Ticket”: Your Certificate of Eligibility (COE)

The only official way to prove to a lender that you meet the service requirements is by obtaining your Certificate of Eligibility (COE). Think of this as your “golden ticket” to the VA loan program.

Many veterans worry that they need to hunt down old paperwork or navigate the VA portal alone to get this document. Here is the good news: When you work with Midwest Family Lending, we can often pull your COE for you instantly through our lender portal. If you are wondering about your status, contact our team today, and let us do the heavy lifting for you.

Detailed Service Duration Requirements

Because service requirements vary based on the era in which you served, we have compiled this table to help you determine if you likely qualify based on your timeline.

| Service Era / Period | Minimum Service Requirement |

|---|---|

| World War II, Korean War, Vietnam War | 90 total days |

| Gulf War (Aug 2, 1990 – Present) | 24 continuous months OR the full period (at least 90 days) for which you were called to active duty. |

| Peacetime Periods (1947-1950, 1955-1964, 1975-1980/81) | 181 continuous days |

| Separated from Service (Active Duty) | 24 continuous months OR the full period (at least 181 days) for which you were called. |

| Selected Reserves / National Guard | 6 creditable years of service. |

Financial Requirements: Credit, Income, and Assets

While the VA guarantees a portion of the loan, they do not lend the money directly. Private lenders—like Midwest Family Lending—provide the funds. This means you must also meet the lender’s financial criteria to ensure you can repay the mortgage.

Credit Score

The VA does not set a minimum credit score, but most lenders look for a score of 620 or higher. However, because we are an independent mortgage broker in Urbandale, we have access to multiple lenders and loan options. This gives us the flexibility to work with veterans who might have unique credit situations. If you aren’t sure where your credit stands, do not disqualify yourself! Get pre-qualified with us to see where you stand.

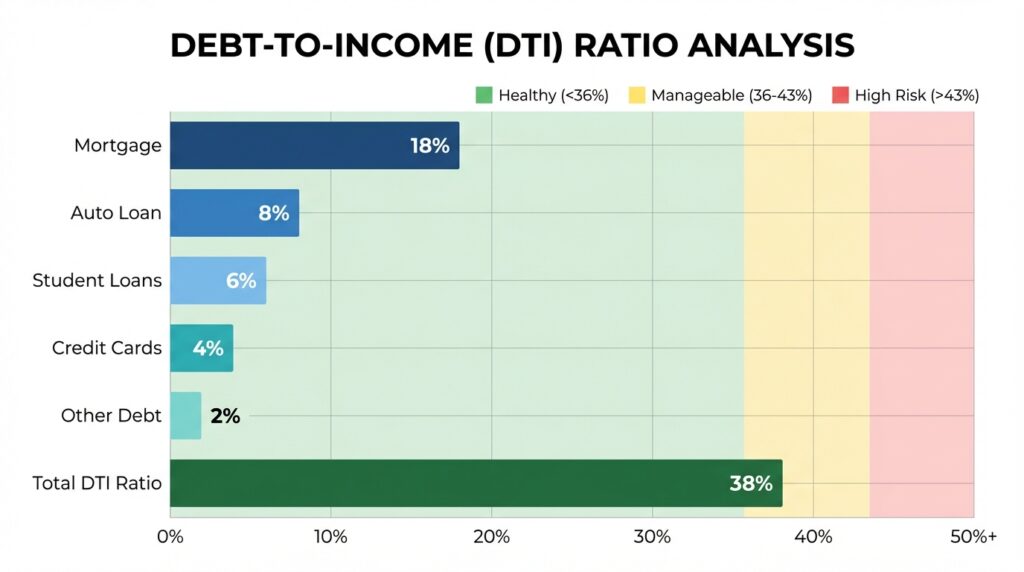

Debt-to-Income (DTI) Ratio

Residual Income

This is a unique requirement for VA loans. The VA wants to ensure that after paying your mortgage and major debts, you have enough money left over for living expenses (food, gas, utilities). This calculation varies by region and family size. Our team of licensed home loan originators are experts at calculating this to ensure your loan file is bulletproof.

Property Requirements in Iowa

The VA loan is designed for primary residences. You generally cannot use a VA loan to buy a rental property or a vacation home (unless you plan to live in it full-time). Whether you are looking at a house in Urbandale, a condo in Des Moines, or an acreage in rural Polk County, the property must meet the VA’s Minimum Property Requirements (MPRs).

These requirements ensure the home is safe, sanitary, and structurally sound. This protects you from buying a “money pit.” Common MPR checks include:

- Functioning heating and electric systems.

- Good roofing with no major leaks.

- No lead-based paint hazards (common in older Iowa homes).

- Access from a public or private street.

Why Choose a Local Urbandale Mortgage Broker?

You have options when choosing a lender, but working with a local expert makes a difference. Big banks and online call centers often treat you like a number. At Midwest Family Lending, we treat you like family. We are proud to have earned a 5-star reputation because we are trustworthy, experienced, and deeply connected to the Urbandale community.

Our team understands the local real estate market. We work directly with local realtors and appraisers to ensure your VA loan closes on time. When you call us, you get a real person—not an automated menu. We are dedicated to simplifying the process and guiding you toward the perfect loan.

Frequently Asked Questions (FAQs)

1. Can I use a VA loan more than once?

Yes! The VA home loan benefit is not a one-time use program. Once you pay off your existing VA loan and dispose of the property (or refinance it into a non-VA loan), your entitlement can be restored. In some cases, you can even have two VA loans at once if you are relocating. We can check your bonus entitlement to see what is possible.

2. Is there a maximum loan limit for VA loans in Iowa?

For veterans with their full entitlement available, there is no loan limit. You can borrow as much as a lender is willing to approve based on your income and credit. This is a huge advantage for buying in higher-priced markets.

3. Do I have to pay for Private Mortgage Insurance (PMI)?

No. This is one of the biggest money-saving features of the VA loan. Unlike FHA or Conventional loans with low down payments, VA loans never require monthly PMI. This can save you hundreds of dollars every month.

4. What is the VA Funding Fee?

The VA Funding Fee is a one-time government fee applied to the loan to help keep the program running for future generations. The amount depends on your down payment and if you’ve used the benefit before. Important: Veterans receiving compensation for a service-connected disability are usually exempt from paying this fee.

5. Can I get a VA loan if I have a bankruptcy or foreclosure in my past?

Yes, and often sooner than with other loan types. Generally, you may qualify for a VA loan two years after a Chapter 7 bankruptcy discharge or a foreclosure. We can help review your specific credit history to see if you are ready to buy.

Ready to Use Your Benefits? Let’s Get Started!

You served our country; now let us serve you. Determining your eligibility is the first step toward owning your dream home in Urbandale or the surrounding Des Moines area. Don’t let uncertainty stop you—our team is here to pull your COE, review your financials, and get you pre-approved.

Midwest Family Lending is here to help you get your ducks in a row. Whether you are ready to buy now or just starting to plan, contact us today.

Apply Now | Contact Us | Call our Urbandale Office: (515) 252-7107

Midwest Family Lending Corporation

2753 99th St, Urbandale, IA 50322

NMLS #4622

www.midwestfamilylending.com

Disclaimer: Midwest Family Lending is not affiliated with or acting on behalf of or at the direction of FHA, VA, USDA, or the Federal Government. All loan programs are subject to credit approval and property requirements.