Unlock the door to homeownership with zero down payment options in Iowa and the Upper Midwest.

Buying a home is the American Dream, but for many potential homebuyers in Urbandale, IA, and the surrounding rural communities, the biggest hurdle standing in the way is the down payment. Saving up 20%, or even 3.5%, of a home’s purchase price can feel overwhelming while managing rent and daily expenses.

But what if you didn’t need a down payment at all? What if you could buy a home just outside the bustling Des Moines metro area with 100% financing?

Enter the USDA Rural Development Loan. Often considered one of the best-kept secrets in the mortgage industry, this program is designed to boost homeownership in rural areas. At Midwest Family Lending, we specialize in helping families navigate these government-backed programs to find the perfect financial fit. Whether you are looking for your first starter home or your forever home, understanding USDA eligibility could save you thousands of dollars upfront.

What Exactly Is a USDA Loan?

A USDA loan is a mortgage loan guaranteed by the U.S. Department of Agriculture. The program’s primary goal is to improve the economy and quality of life in rural America by offering affordable financing options to low-to-moderate-income families.

Because the government guarantees a portion of the loan, lenders like Midwest Family Lending can offer more favorable terms, such as zero down payment and lower interest rates, to borrowers who might not qualify for conventional financing.

It’s Not Just for Farmers

One of the biggest misconceptions about the USDA loan is that you have to buy a working farm or live in the middle of nowhere to qualify. This is simply not true. The USDA’s definition of “rural” is surprisingly broad. Many suburban towns just outside of major cities like Des Moines, Omaha, or Sioux Falls often qualify.

If you are looking to buy a home in a smaller community or on the outskirts of Urbandale, you might be sitting on a goldmine of eligibility without even knowing it.

The Top Benefits of a USDA Rural Development Loan

Why should you consider a USDA loan over an FHA or Conventional loan? Here are the standout benefits that make this program a favorite among our clients:

- 100% Financing (No Down Payment): This is the headline feature. Unlike FHA loans (which require 3.5% down) or Conventional loans (often 3-20% down), a USDA loan allows you to finance the entire purchase price of the home.

- Lower Mortgage Insurance Costs: While USDA loans do require mortgage insurance (an upfront fee and an annual fee paid monthly), the rates are historically lower than those for FHA loans. This keeps your monthly payment more affordable.

- Competitive Interest Rates: Because the loan is backed by the government, lenders can often offer rates that are lower than the market average for conventional loans.

- Flexible Credit Guidelines: While a good credit history helps, the USDA program can be more forgiving regarding credit scores compared to strict conventional requirements.

- Seller Concessions: The seller can contribute up to 6% of the sale price toward your closing costs, potentially allowing you to move in with little to no money out of pocket.

Am I Eligible? Understanding the Requirements

To take advantage of this program, you need to meet specific criteria regarding the property, your income, and your creditworthiness. At Midwest Family Lending, our team of experienced mortgage experts can help you verify your eligibility quickly.

1. Property Eligibility (The “Rural” Factor)

The home must be located in a USDA-eligible area. Generally, this includes open country and towns with a population of fewer than 35,000 people. In Iowa, vast stretches of the state are eligible. Even parts of Dallas County and areas surrounding the Des Moines metro can qualify.

Tip: Don’t assume a home is ineligible just because it’s near a city. Ask us to check the address for you!

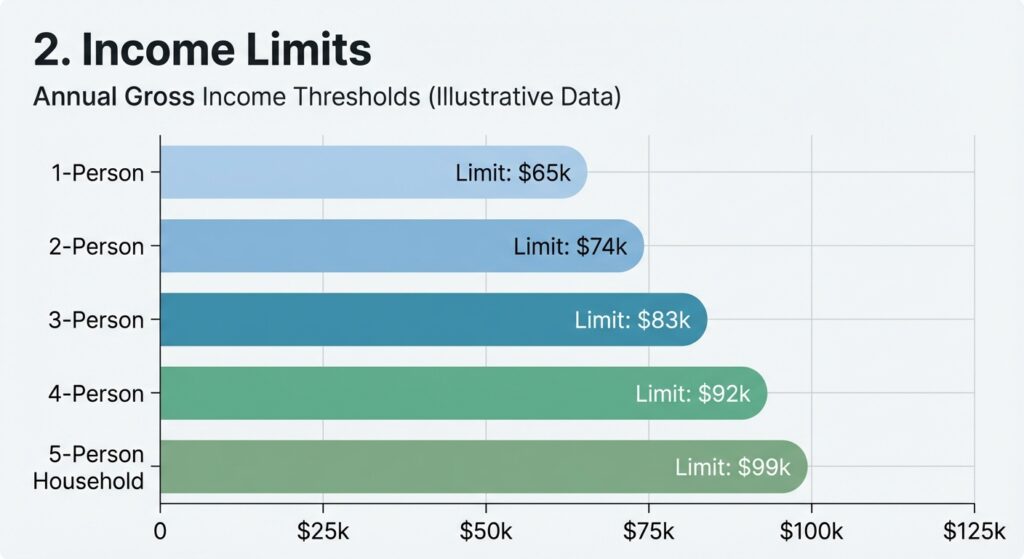

2. Income Limits

The USDA loan is a means-tested program, meaning it is designed for low-to-moderate-income households. There are strict income caps based on the size of your household and the county where you are buying. If you earn too much, you may not qualify for this specific program, but we can help you explore other loan options.

Income calculations can be tricky because they include the income of all adult household members, not just the borrowers. However, there are deductions for childcare expenses, dependents, and elderly care that can help you stay under the limit.

3. Credit and Employment

While there is no fixed minimum credit score set by the USDA, most lenders look for a score of at least 640 for a streamlined approval process. You must also demonstrate a stable employment history, typically two years of consistent work.

Loan Comparison: USDA vs. FHA vs. Conventional

| Feature | USDA Loan | FHA Loan | Conventional Loan |

|---|---|---|---|

| Down Payment | 0% | 3.5% | 3% – 20% |

| Mortgage Insurance | Lower rates (Upfront & Annual) | Higher rates (Upfront & Annual) | PMI required if under 20% down |

| Location Requirement | Must be in Eligible Rural Area | No restrictions | No restrictions |

| Income Limits | Yes (Maximum income caps) | No | No |

| Credit Flexibility | Moderate | High | Strict |

Not sure which numbers work for your budget? Try our free mortgage calculators to estimate your monthly payments.

Why Work with a Local Mortgage Broker in Urbandale?

When dealing with government-backed loans like the USDA Rural Development program, experience matters. The guidelines can be complex, and having a team that knows the local landscape is invaluable.

Midwest Family Lending isn’t just a lender; we are your neighbors. We have been serving the community for over 25 years, helping families in Iowa, Nebraska, South Dakota, and Colorado say “Yes” to their dreams.

- We Are Trustworthy: We have earned a 5-star reputation because we treat our customers like family. We look out for your best interests, not just the bottom line.

- We Are Fast & Responsive: In a competitive housing market, time is money. We work proactively to keep you ahead of schedule.

- We Are Connected: Real estate professionals recommend us because we have a track record of making “mortgage magic” happen behind the scenes.

Furthermore, we believe in giving back. Through our MFLCares initiative, we support local charities like the Huntington’s Disease Society of America – Iowa Chapter. When you work with us, you are supporting a business that supports your community.

Steps to Apply for a USDA Loan

- Get Your Ducks in a Row: The first step is a consultation. Contact us to discuss your goals and financial situation.

- Pre-Qualification: Complete our quick pre-qualification form. This gives us the data we need to check your income eligibility and credit.

- Property Search: Once you know your budget and eligible areas, you can start house hunting with a real estate agent. We can recommend trusted local agents if you need one!

- Application & Processing: Once you make an offer, we handle the heavy lifting—verifying documents, ordering the appraisal, and submitting your file to the USDA for approval.

- Closing: We guide you to the finish line so you can pick up your keys!

Frequently Asked Questions (FAQs)

1. Do I have to be a first-time homebuyer to use a USDA loan?

No! While USDA loans are fantastic for first-time buyers because of the zero down payment requirement, you do not have to be a first-time buyer to qualify. However, you generally cannot own another adequate home in the local area at the time of closing.

2. Can I use a USDA loan to refinance my current home?

Yes, but only if you currently have a USDA loan. The USDA offers a Streamlined Assist Refinance program that allows existing USDA borrowers to refinance for a lower interest rate with very little paperwork and often no appraisal. If you want to refinance a different type of loan into a USDA loan, it is more complex and subject to current restrictions.

3. What are the closing costs for a USDA loan?

Closing costs vary, but they typically range from 2% to 5% of the purchase price. The great news is that USDA loans allow the seller to pay up to 6% of the sale price toward your closing costs. Additionally, if the home appraises for more than the sale price, you may be able to roll some closing costs into the loan amount.

4. How strict are the inspection requirements?

The USDA requires the home to be safe, sanitary, and structurally sound. The appraisal acts as a basic check for these standards. If the appraiser flags issues like a failing roof or peeling paint (on homes built before 1978), those repairs must usually be completed before the loan can close.

5. Is there a maximum loan amount?

Unlike FHA or Conventional loans, the USDA does not have a set maximum loan limit. Instead, your loan amount is determined by your ability to repay the loan (your debt-to-income ratio) and the applicable income limits for your household size.

Ready to Make Your Move?

Don’t let the fear of a down payment keep you renting for another year. The USDA Rural Development loan might be the key to unlocking your new front door.

At Midwest Family Lending, we are dedicated to simplifying the process and guiding you toward the perfect loan. You deserve to feel confident and in control of the biggest purchase of your life.

Let’s get started today!

Apply Now to Check Your Eligibility

or

Find a Licensed Home Loan Originator Near You

Midwest Family Lending

Address: 2753 99th St, Urbandale, IA 50322

Phone: (515) 252-7107

Email: info@midwestfamilylending.com

Midwest Family Lending Corporation NMLS #4622. Equal Housing Lender. This content is for educational purposes and does not constitute a commitment to lend. Programs, rates, and terms are subject to change without notice.